Public credit spreads sit near decade lows, with little cushion for deterioration.

Equity indices carry concentration risk that undermines the diversification investors assume they own. Long-duration fixed income offers negative real yield once inflation is accounted for.

The traditional balanced portfolio is no longer diversified in the way it was designed to be – which makes short-duration, asset-backed income the more defensible place to allocate.

Our Principles

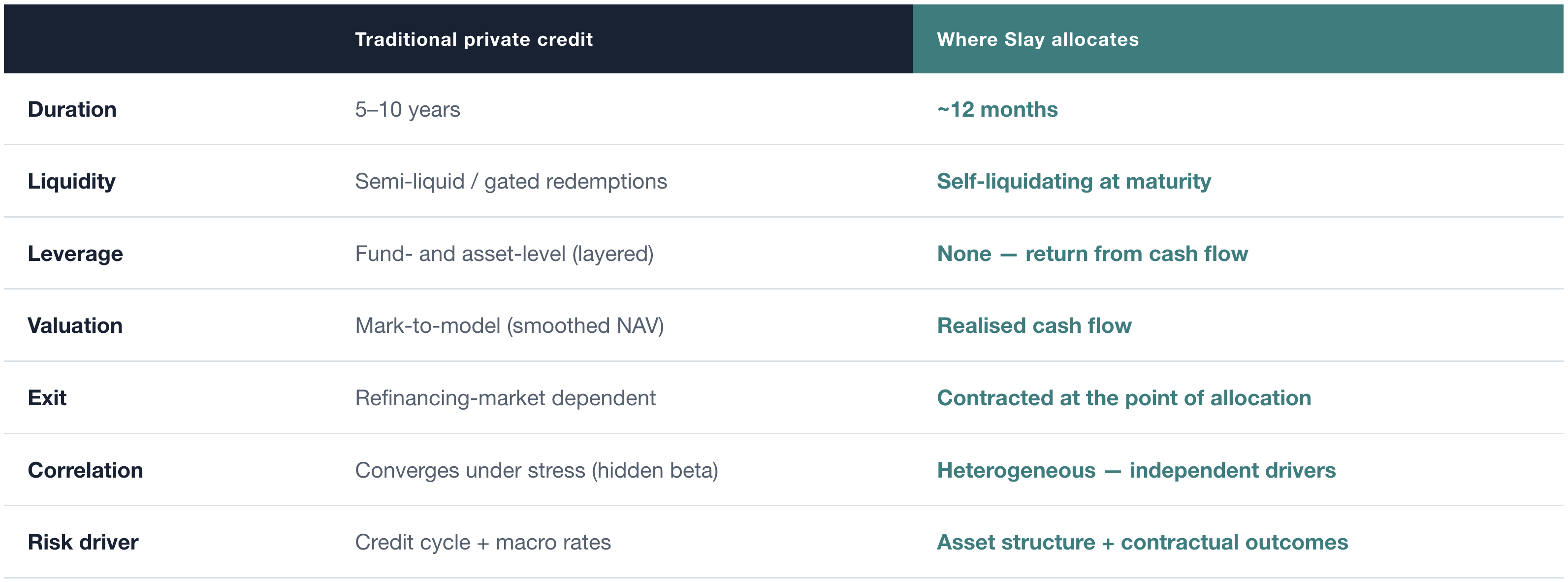

1. Short Tenor

Typically 12-18 months. Capital recycles continuously, with no multi-year credit-cycle exposure.

2. Stable Yield

Income governed by contractual terms and paid on a defined schedule. Cash in hand, not on paper.

3. Tangible Collateral

Every position secured against independently valued hard assets and contractual cash flows.

4. Decorrelated

Independent cash flow drivers across sectors and geographies, providing insulation from public market volatility.

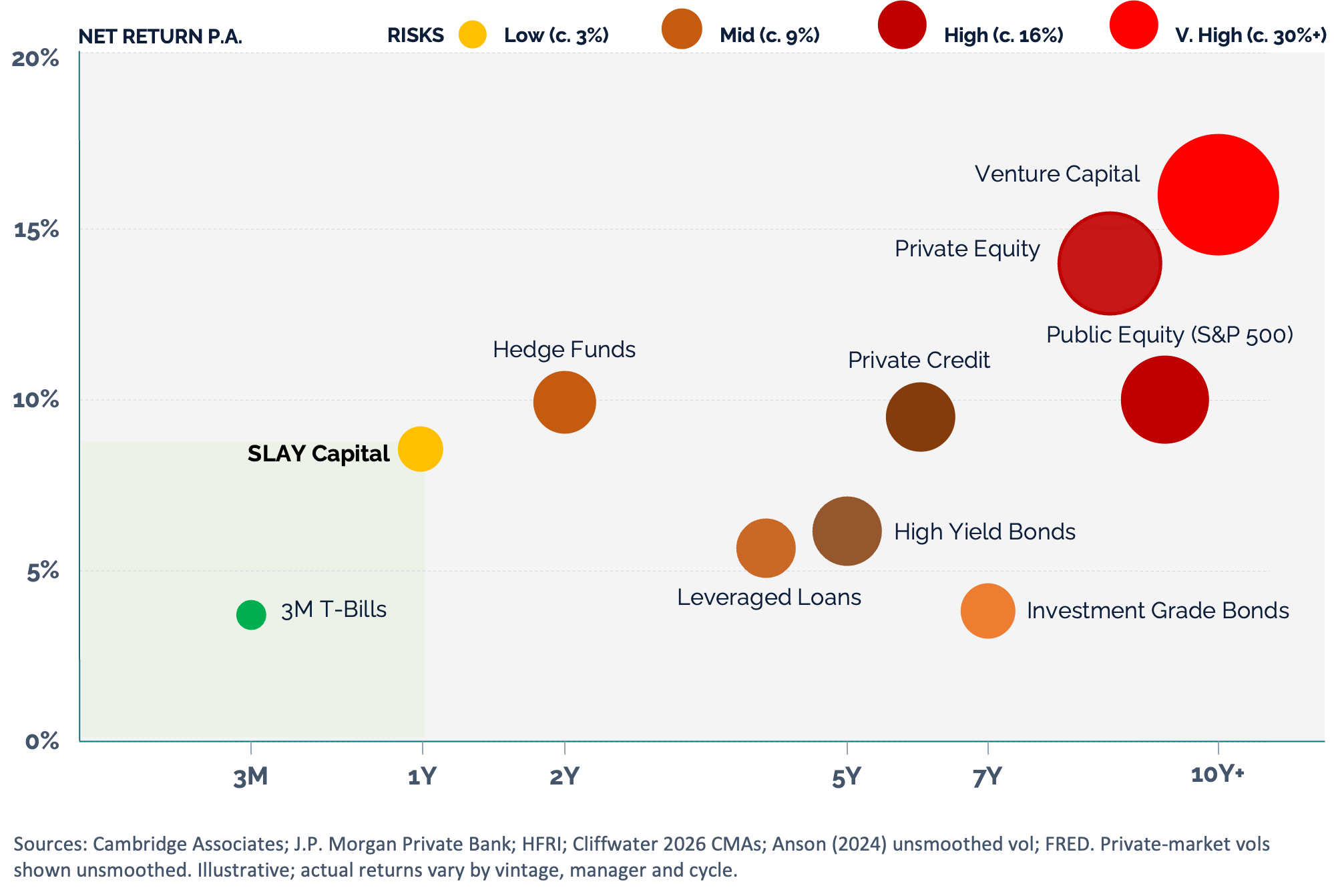

Where We Allocate

We target positions that combine institutional-grade yield with short tenor and low realised volatility – a profile conventional asset classes rarely offer together.

Treasury bills are the only genuinely lower-risk comparable, and they yield a fraction of the return while carrying reinvestment risk at every rollover. Higher-yielding strategies carry many times the volatility and far longer lock-ups.

On a risk-adjusted, tenor-adjusted basis, this is a structurally underserved part of the market – and we allocate there deliberately.

Our Preferred Sectors

Global Trade Finance

Trade finance delivers structured working-capital funding at key points in global supply chains. These short-tenor facilities are typically secured against goods, receivables, or insured trade flows, offering diversified exposure, strong downside protection, and predictable capital turnover.

Real Estate Finance

Mortgage bonds offer exposure to securitized pools of prime property loans, secured by legal claims over underlying real estate. These structures are designed to deliver stable, income-focused returns backed by tangible collateral.

Embedded Finance

Receivables funding integrated within major e-commerce ecosystems. Capital is deployed into high-frequency, secured cash flows with short-duration exposure; generating recurring revenue streams.

Aviation and Maritime Finance

Specialist lending and leasing for aircraft and vessels, secured by legal title to high-value mobile assets. Strong contractual protections support a resilient, asset-backed strategy designed to deliver stable, predictable cash flows with downside protection.

Insurance Linked Securities

A diversified allocation to insurance linked securities (ILS) including catastrophe bonds and collateralised reinsurance — that underwrites clearly defined, remote insurance risks. A meaningful portfolio diversification tool with return streams that has low correlation to traditional financial markets.

How We Manage Risks

We do not claim to eliminate risks – only to know which risks are removed by structure, and which remain to be managed by discipline before we allocate capital.

This is the standard every position clears before we commit capital.

Where a structure does not meet them, we do not allocate.

Removed by Design

- Duration risk is contained by short tenors.

- Refinancing dependency is removed by contracting the exit at the point of allocation.

- Leverage is removed entirely – return comes from cash flow, not borrowing.

- Valuation opacity is removed by relying on realised cash flow rather than mark-to-model.

- Trapped-capital risk is removed by self-liquidation, with no redemption gates.

- And concentration is diluted across sectors, geographies and cash-flow mechanisms.

Managed by Discipline

- Cash-flow timing can slow across positions simultaneously under stress; we manage this through genuine diversity of underlying economic activity.

- Counterparties can prove more linked than they appear; we manage this through concentration limits and quality thresholds set before we allocate.

- Legal and settlement risk is addressed deal by deal, through defined collateral segregation and enforcement rights reviewed by counsel in the relevant jurisdiction.

Structurally Distinct by Design

The same exposures, selected against a different standard – short duration, self-liquidating, unlevered.

Returns governed by asset structure and contractual outcomes, not by the credit cycle and level of rates.

Built to avoid the failure modes of traditional private credit.

Reach out to us via the contact page to find out more.